Top Fair Credit Loan Lenders Reviewed

What is a Fair Credit Score?

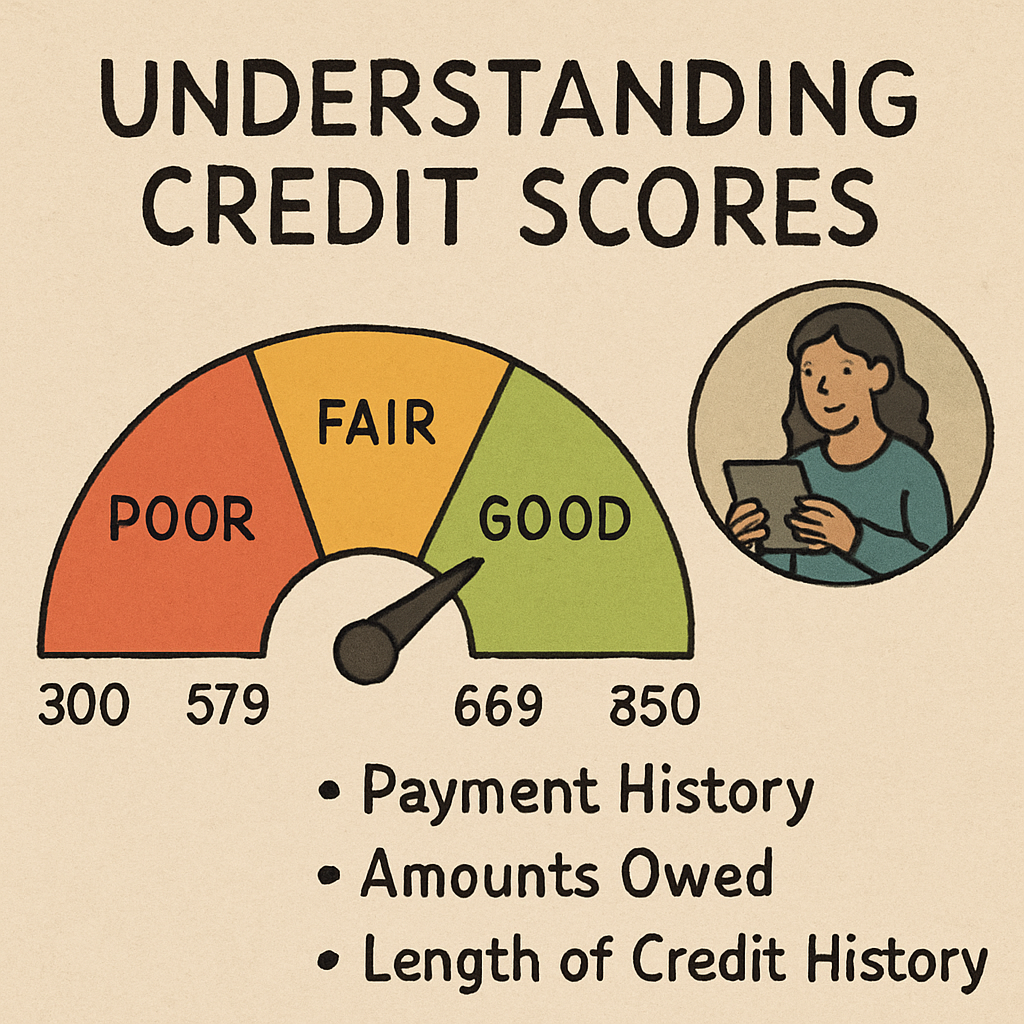

Before diving into lenders, it’s crucial to understand what constitutes a fair credit score. Typically, a fair credit score ranges from 580 to 669 on the FICO scale. This range sits between poor and good credit scores, providing a moderate level of creditworthiness. While this score might not secure the best interest rates, it can still grant you access to a variety of loan products, offering more options than someone with a poor credit score.

Understanding where your credit score stands is the first step in navigating the loan landscape. By knowing your score, you can set realistic expectations regarding the types of loans available to you and the interest rates you might encounter. Moreover, being aware of your credit score category can help you identify areas for improvement, potentially increasing your options in the future.

Why Your Credit Score Matters

Your credit score is a numerical representation of your creditworthiness, impacting your ability to secure loans and the terms of those loans. Lenders use this score to evaluate the risk of lending to you. A higher score often translates to better terms, such as lower interest rates and higher loan amounts. Conversely, a lower score might limit your options and result in higher costs over the loan’s life.

Understanding your credit score can help you better navigate the loan application process. It provides insight into how lenders view you as a borrower and what you can do to improve your standing. By knowing the factors that affect your score, such as payment history and credit utilization, you can make informed decisions to enhance your credit profile over time.

Factors Influencing Your Credit Score

Several factors contribute to your credit score, each carrying a different weight. Payment history is the most significant factor, accounting for about 35% of your score. This includes your record of on-time payments and any instances of late or missed payments. Consistently paying bills on time can positively impact this aspect of your score.

Credit utilization, or the amount of credit you’re using compared to your total credit limit, is another crucial factor. Keeping your credit utilization below 30% is generally recommended for a healthy credit score. Other elements include the length of your credit history, the types of credit in use, and recent credit inquiries. Understanding these factors allows you to strategically manage your credit habits to improve your score.

Top Lenders for Fair Credit Loans

Here, we’ll explore some of the best lenders offering loans for fair credit. Each lender has its unique offerings, so it’s vital to compare to find the best fit for your needs.

LendingClub

LendingClub is a peer-to-peer lending platform that connects borrowers with investors. It’s known for its flexibility and competitive rates for those with fair credit. Borrowers can benefit from a wide range of loan amounts, making it a versatile option for different financial needs.

Key Features:

- Loan amounts: $1,000 – $40,000

- APR range: 8.05% – 35.89%

- Loan terms: 36 or 60 months

- No prepayment penalty

LendingClub’s application process is straightforward. You can check your rate without affecting your credit score, which is an advantage for those still shopping around. This soft inquiry ensures that your credit score remains intact while you explore your options. Additionally, LendingClub provides personalized loan offers based on your financial profile, enhancing the borrowing experience.

Avant

Avant is a popular choice for borrowers with fair credit. It offers a straightforward application process and quick funding, making it a convenient option. The platform is designed to cater to those who may not have a perfect credit history but still seek access to personal loans with reasonable terms.

Key Features:

- Loan amounts: $2,000 – $35,000

- APR range: 9.95% – 35.99%

- Loan terms: 24 to 60 months

- Administration fees: Up to 4.75%

Avant’s flexible credit requirements and user-friendly online platform make it a go-to for many seeking personal loans for fair credit. Its quick approval process and easy-to-navigate website simplify the borrowing process, allowing you to receive funds in a timely manner. Furthermore, Avant provides educational resources to help borrowers better understand their credit profiles and improve their financial standing.

Upstart

Upstart leverages artificial intelligence to assess loan applications, considering factors beyond just your credit score, such as education and job history. This innovative approach allows Upstart to offer more tailored loan options, potentially resulting in more favorable terms for eligible borrowers.

Key Features:

- Loan amounts: $1,000 – $50,000

- APR range: 6.18% – 35.99%

- Loan terms: 36 or 60 months

- No prepayment penalty

This approach can be beneficial for borrowers with a strong educational background or a stable employment history, offering more competitive rates. By considering a broader range of factors, Upstart provides opportunities for those who might be overlooked by traditional lenders. This holistic assessment can lead to better loan terms, particularly for individuals who have recently graduated or started a new career path.

Other Notable Lenders

In addition to LendingClub, Avant, and Upstart, several other lenders offer competitive options for fair credit borrowers. Companies like Prosper and Best Egg provide personal loans with varying terms and conditions, catering to different financial needs and credit profiles. It’s essential to research and compare these lenders to find the best fit for your situation.

Prosper, for instance, offers a peer-to-peer lending platform similar to LendingClub, with a focus on personalized service and flexible loan options. Best Egg, on the other hand, emphasizes quick funding and straightforward terms, making it a viable choice for those in need of fast financial solutions. Exploring these alternatives can expand your options and help you secure a loan that aligns with your goals.

Considerations Before Applying

by iMattSmart (https://unsplash.com/@imattsmart)

Interest Rates and Fees

When comparing loans, always consider the APR, which includes both the interest rate and any fees. A lower APR means less money paid over the life of the loan. It’s crucial to understand the full cost of borrowing, as some loans may have hidden fees that can increase the total amount paid.

In addition to the interest rate, look for any origination fees or administrative charges that might apply. These fees can add up, impacting the overall affordability of the loan. By carefully reviewing the APR and associated costs, you can make a more informed decision and select a loan that fits your budget.

Loan Terms

Loan terms, such as the repayment period, can significantly impact your monthly payments and total interest paid. Longer terms may offer lower monthly payments but often result in higher total interest. It’s important to balance your monthly budget with the overall cost of the loan.

Consider how the loan term aligns with your financial goals. If you anticipate an increase in your income or have a strategy to pay off the loan early, a shorter term might be more advantageous. However, if cash flow is a concern, opting for a longer term with manageable payments could be a better fit. Understanding the implications of different loan terms can help you choose a repayment plan that aligns with your financial situation.

Prepayment Penalties

Some lenders charge a fee if you pay off your loan early. If you anticipate being able to do so, look for lenders that do not impose these penalties. Prepayment penalties can negate the benefits of paying off a loan ahead of schedule, so it’s essential to be aware of these conditions before committing to a lender.

Research lenders that offer flexible repayment options without penalties, allowing you to pay down your debt faster if your financial situation improves. This flexibility can save you money on interest and reduce the overall loan cost. By choosing a lender that aligns with your financial strategy, you can maintain control over your repayment plan.

Eligibility Requirements

Each lender has specific eligibility criteria that borrowers must meet to qualify for a loan. These requirements often include a minimum credit score, income level, and debt-to-income ratio. Understanding these criteria can help you determine which lenders are most likely to approve your application.

Some lenders may also consider additional factors, such as employment history and educational background, when assessing eligibility. By reviewing and understanding these requirements, you can focus your efforts on lenders that align with your financial profile, increasing your chances of approval.

Tips for Improving Your Loan Prospects

Improving your credit score can open doors to better loan options. Here are some strategies to enhance your credit profile:

Pay Bills on Time

Consistently paying your bills on time is one of the most effective ways to boost your credit score. Set up automatic payments or reminders to help manage due dates. Timely payments demonstrate financial responsibility and can positively impact your payment history, which is the most significant factor in your credit score.

If you have missed payments in the past, focus on building a consistent track record moving forward. Over time, your payment history will improve, leading to a better credit score. Additionally, consider contacting creditors to negotiate payment plans if you’re facing financial difficulties, as this can prevent negative marks on your credit report.

Reduce Debt

Lowering your credit card balances can positively impact your credit utilization ratio, a key component of your credit score. Aim to keep your credit utilization below 30% to maintain a healthy credit profile. Paying down existing debt not only improves your credit score but also reduces the interest you pay over time.

Develop a debt repayment plan that prioritizes high-interest debt first, freeing up more funds to tackle other balances. This strategy, known as the avalanche method, can accelerate your debt reduction efforts. Alternatively, the snowball method focuses on paying off smaller balances first, providing psychological motivation as you see progress.

Check Your Credit Report

Regularly review your credit report for errors or discrepancies. Correcting these can sometimes provide a quick boost to your score. You’re entitled to a free credit report from each of the three major credit bureaus annually, which you can access through AnnualCreditReport.com.

Look for inaccuracies such as incorrect account information, duplicate entries, or fraudulent accounts. Disputing these errors with the credit bureau can lead to corrections that improve your score. Staying informed about your credit report ensures that your score accurately reflects your creditworthiness.

Limit New Credit Inquiries

Each new credit inquiry can slightly decrease your score. Be strategic about when and where you apply for new credit. While inquiries have a relatively small impact on your score, accumulating several in a short period can raise red flags for lenders.

If you plan to apply for multiple loans or credit products, try to do so within a short time frame. This way, credit inquiries can be grouped together, minimizing their impact on your score. Focus on applying for credit only when necessary, and prioritize lenders that perform soft inquiries during the pre-approval process.

Build a Strong Credit History

A longer credit history generally benefits your credit score. If you’re new to credit, consider starting with a secured credit card or becoming an authorized user on an existing account. These options can help you establish credit and build a positive payment history.

Over time, maintaining good credit habits, such as timely payments and low credit utilization, will contribute to a strong credit history. As your credit profile matures, you’ll gain access to better loan terms and financial opportunities.

Conclusion

Navigating loans with a fair credit score doesn’t have to be daunting. With numerous lenders offering competitive terms, you can find a loan that meets your financial needs. By understanding your credit score and exploring various lenders, you can make informed decisions that align with your financial goals. Remember, improving your credit score over time can lead to even better loan opportunities in the future.

By taking proactive steps to enhance your credit profile, you can increase your chances of securing favorable loan terms. Stay informed about your credit report, adopt responsible financial habits, and explore different lending options to find the best fit for your situation. With dedication and strategic planning, you can achieve your financial objectives and enjoy greater financial flexibility.